The most important financial story right now may not be tariffs. It may be what’s sitting behind them.

Trump’s Beijing trip was framed publicly as trade. But the market signals underneath it point to something bigger: a possible attempt to weaken the dollar through gold, investment flows, and industrial policy instead of a direct currency deal.

I don’t know if that deal gets done. Nobody outside the room does. But the fingerprints are worth watching.

What the Data Shows

The dollar has been weakening since late March, but not in the way a normal trade-war setup would suggest. If the goal were simply to pressure China, I’d expect more focus on the yuan. Instead, the cleaner signal has been gold.

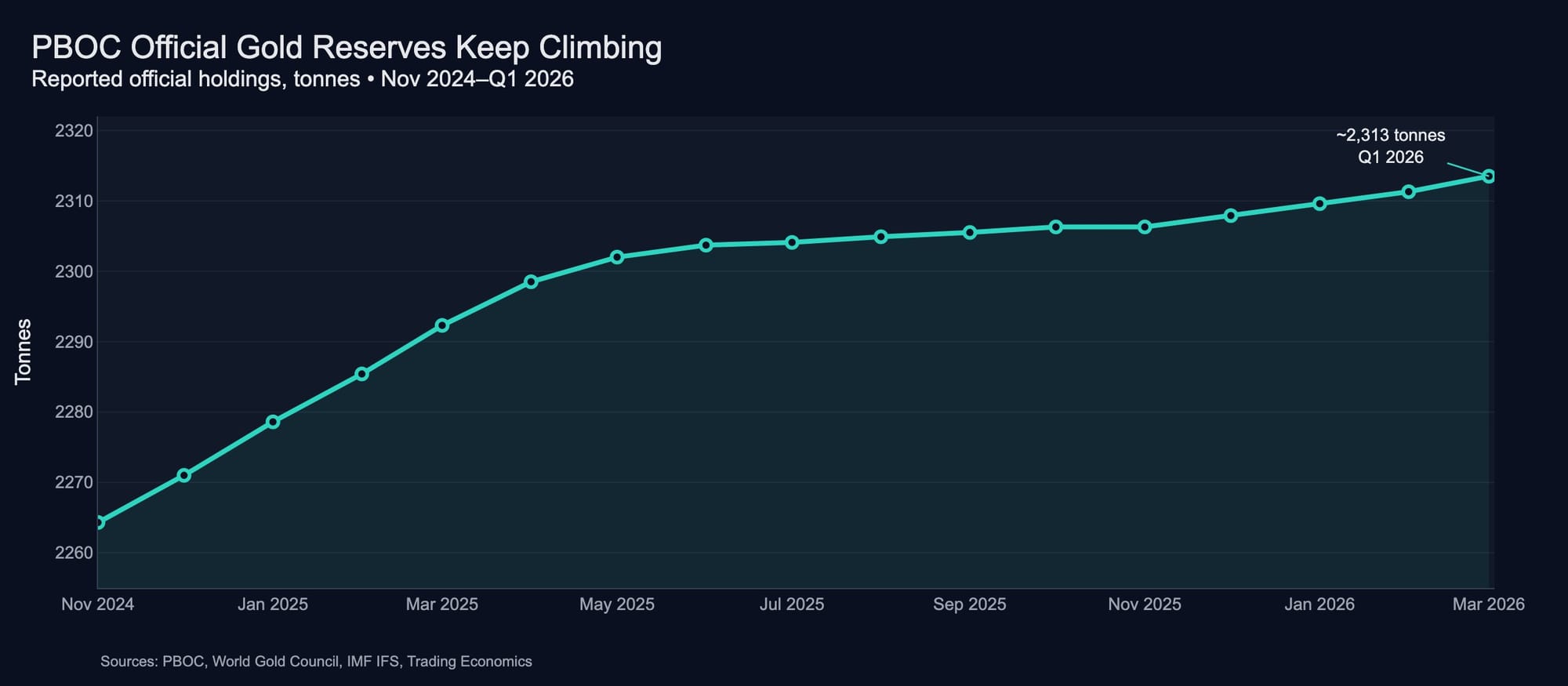

China’s official gold reserves have kept rising. World Gold Council and PBOC data show China’s reported holdings reaching roughly 2,313 tonnes by Q1 2026 after a long stretch of steady central-bank buying.

That reported number may understate the full picture. Goldman Sachs and Societe Generale have both estimated that China’s true gold accumulation could be higher than the official IMF-reported figure because some purchases can move through domestic channels.

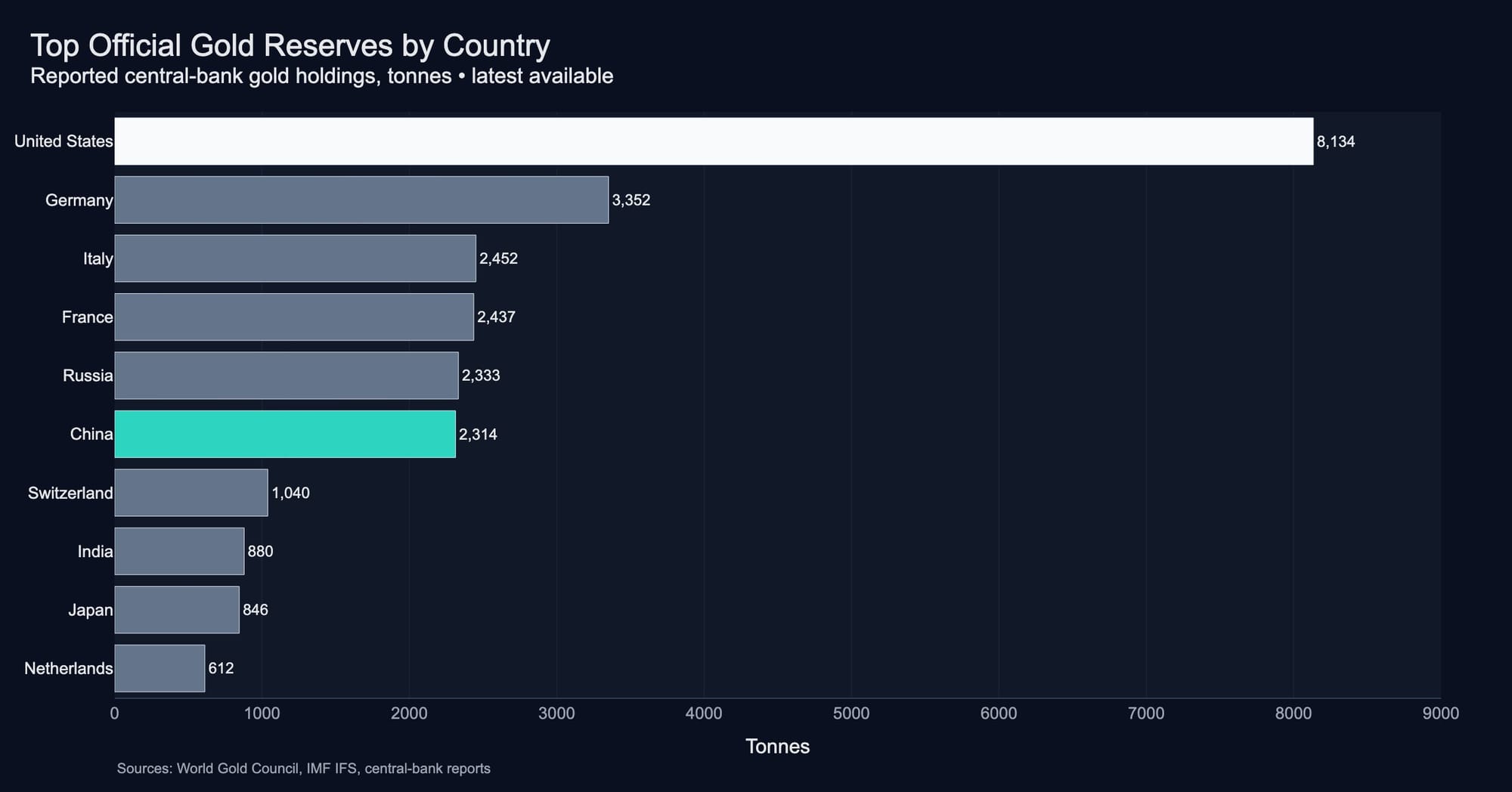

On the global leaderboard, the US still dominates with more than 8,100 tonnes of official gold reserves. China is nowhere close to the US on reported holdings. But the pace of accumulation is the story, not the current ranking.

Why It Matters for Portfolios

If a managed dollar devaluation is underway — intentional or not — scarce assets matter more.

Gold is the obvious one. Bitcoin is another. Real estate, commodities, and productive businesses with pricing power usually hold up better than cash when purchasing power erodes.

That doesn’t mean every hard asset is automatically a buy. It means cash becomes harder to defend if the policy direction is a weaker dollar.

I’m not in a commodity position right now. But I’m watching this closely because if this theory has legs, it changes the context for everything else I hold.

What I’m Watching

The cleanest confirmation would be a formal US-China manufacturing investment framework with real dollar figures attached.

A large commitment tied to factories, supply chains, and industrial buildout would be the public signal that something larger may have been agreed behind closed doors. If gold keeps running while the dollar keeps weakening — and the Fed does not move aggressively to reverse it — the theory gets harder to ignore.

Until then, this is still a theory. A well-supported one, but still a theory.

The Deep Note — The Full Dollar-Gold Theory

A note before you read: Everything below is speculative. The framework is real, the data points are real, and the historical parallel is real. But the deal being described has not been confirmed.

The 1985 Blueprint

In 1985, the US had a trade deficit problem and a dollar that was too strong for American manufacturers to compete globally.

The Reagan administration held a closed-door meeting at the Plaza Hotel in New York with France, West Germany, Japan, and the UK. The agreement they reached — the Plaza Accord — coordinated currency intervention to weaken the dollar against major currencies, especially the Japanese yen and German mark.

The yen roughly doubled against the dollar over the following years. Japanese exports became more expensive. American goods became more competitive. The trade deficit eventually improved.

Japan also got something in return: deeper access to invest in the US. Japanese capital moved into factories, real estate, and treasuries. Toyota, Honda, and Nissan expanded their American manufacturing footprints.

For a brief window, everyone appeared to win.

Then Japan’s export-driven economy took the hit from the currency shock. To offset it, policymakers flooded the system with cheap money. That helped create one of the largest asset bubbles in modern history.

When it burst, Japan spent decades digging out. History remembers that period as the Lost Decades.

Why China Won’t Make Japan’s Mistake

China watched what happened to Japan. A direct currency revaluation — forcing the yuan sharply higher against the dollar — is probably the hard line.

But there’s another way to reach a similar outcome without touching the exchange rate directly.

The US government holds more than 8,100 tonnes of gold. On the official books, that gold is still valued at $42.2222 per ounce, according to the US Treasury. The market price is above $3,000.

That means the US is sitting on an asset that is dramatically understated on paper.

Marking gold closer to market would not solve the debt problem by itself. The numbers are too large for that. But it would make the asset side of the balance sheet look less absurdly understated and create political cover for a broader monetary reset.

The key is that the dollar would weaken against gold, not directly against the yuan.

China’s reserves would appreciate too. Both sides get the repricing without the optics of a Plaza-style currency deal.

That would be the mechanism: dollar devaluation routed through gold instead of foreign exchange markets.

What China Gets From a $1 Trillion Investment

Bloomberg and the New York Times have reported discussions around a possible large-scale Chinese investment framework in the US, with numbers as high as $1 trillion being discussed or floated.

The parallel to post-Plaza Japan is obvious: foreign capital building domestic capacity in exchange for access.

But China would not be doing this as charity. What it would be buying is access to the largest consumer economy in the world, a seat at the table in whatever monetary structure comes next, and appreciation on gold reserves it has been accumulating for years.

The US would get manufacturing investment, political cover to claim jobs are coming back, and a weaker dollar that makes parts of the debt load easier to carry over time.

That may be the trade.

Not tariffs. Not just factories. A monetary reset with industrial policy wrapped around it.

The K-Shaped Reality

Whatever the mechanism, the outcome of a managed dollar devaluation is the same: inflation. And inflation does not hit everyone equally.

Asset owners tend to benefit first. Stocks, real estate, gold, Bitcoin, and other scarce assets with real demand usually rise in nominal terms when the currency weakens. Net worth goes up on paper, even if the purchasing-power question is more complicated.

Households sitting mostly in cash, savings accounts, or fixed-rate dollar instruments usually feel the other side. Rent rises. Groceries cost more. Wages often lag. Purchasing power erodes quietly.

The uncomfortable part is that AI is accelerating a similar divide.

The productivity gains from AI compound the position of people who own the tools and companies building them. The job displacement from AI falls disproportionately on the same group already being squeezed by inflation.

Both forces are moving in the same direction, at the same time.

What Would Confirm This

Three things would move this from theory to trade for me.

A formal US-China manufacturing investment deal gets announced with real dollar figures attached. Gold continues running while the dollar keeps weakening. And the Fed does not respond aggressively enough to reverse the move.

None of those have fully happened yet.

All of them are worth watching.

Related reading: [The Smart Money Just Moved Into Alphabet — And It's Not Just Buffett] and [Klarman and Elliott Both Opened NCLH in Q1 — The Stock Is Now at 52-Week Lows]

Howard is a full-time trader based in New Jersey with 13 years of experience across Forex, crypto, equities, and futures. He started Position Note to document his trades and analysis in public. All positions are disclosed. Nothing here is personalized investment advice.

Written by